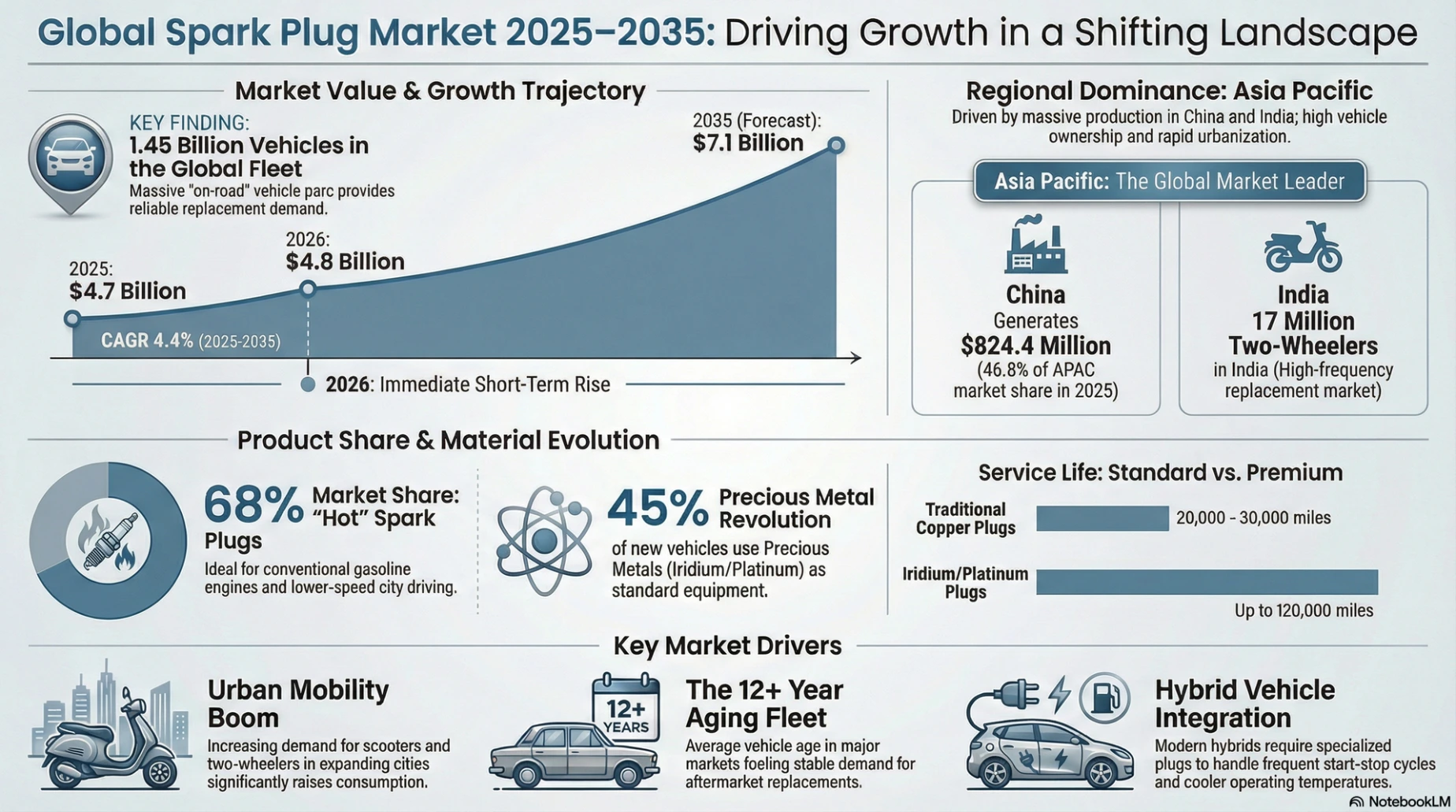

While the automotive world is abuzz with the transition to electric vehicles (EVs), the internal combustion engine (ICE) remains the workhorse of global mobility, ensuring a robust and expanding market for spark plugs. According to comprehensive market analysis, the global automotive spark plug market is estimated at USD 4.7 billion in 2025 and is projected to reach USD 7.1 billion by 2035, growing at a Compound Annual Growth Rate (CAGR) of 4.4% to 5.0% depending on the specific forecast model. This growth is not merely a remnant of the past but a dynamic evolution driven by urbanization, aging vehicle fleets, and the specific demands of hybrid technologies.

The Driving Forces of Market Resilience

1. The Urban Mobility and Two-Wheeler Boom

A critical driver of spark plug demand is the explosion of urban mobility, particularly in the Asia-Pacific region. As of 2024, over 55% of the global population resides in urban areas, necessitating compact, efficient transportation. This has led to a surge in the production and sale of scooters and motorcycles. In India alone, two-wheeler sales exceeded 17 million units in 2024. These vehicles predominantly utilize small gasoline engines that require frequent maintenance. Consequently, "Hot" spark plugs, which are designed to resist fouling in low-speed, stop-and-go traffic by retaining more heat, currently dominate the market with a 68% share.

2. The Aging Global Fleet

The average age of vehicles on the road has surpassed 12 years in 2024. As vehicles age, they exit the warranty period and enter the aftermarket ecosystem, where maintenance falls to independent workshops and DIY owners. This aging fleet creates a consistent, recession-resistant demand for replacement parts. Global aftermarket sales channels currently hold a significant portion of the market, fueled by a vehicle parc (total vehicles in operation) that reached approximately 1.45 billion units in 2024.

3. The Hybrid "Bridge" Technology

While Battery Electric Vehicles (BEVs) eliminate the need for spark plugs, Hybrid Electric Vehicles (HEVs) and Plug-in Hybrids (PHEVs) rely on them heavily. Hybrids present a unique engineering challenge: the internal combustion engine is frequently switched on and off to save fuel. This intermittent operation prevents the engine from consistently maintaining its self-cleaning temperature (approx. 500°C), leading to higher risks of carbon fouling. Manufacturers like Bosch have responded with specific "hybrid-ready" plugs, such as the EVO and Double Iridium Pin-to-Pin series, which feature robust insulators and specialized electrode designs to handle these harsh thermal cycles and high-voltage restarts.

Regional Powerhouses

- Asia Pacific: This region is the undisputed leader, holding an estimated 32.7% to 47% of the market share depending on the segment analysis. China alone accounts for nearly 47% of the Asia Pacific share, driven by a passenger car production volume exceeding 28 million units. The region's demand is characterized by a high volume of copper and standard platinum plugs for the massive two-wheeler and entry-level car markets.

- North America: The U.S. market is defined by a preference for high-performance and durability. With a vehicle fleet age exceeding 12 years and a high prevalence of trucks and SUVs, there is strong aftermarket demand for long-life Iridium and Double Platinum plugs.

- Europe: Germany leads the European market, leveraging its strong OEM network (BMW, Mercedes, VW). The region focuses intensely on premium plugs that support strict Euro emissions standards and fuel efficiency targets.

- Latin America & MEA: Brazil leads Latin American growth with a 4.3% CAGR, driven by flex-fuel engines. In the Middle East, the UAE market is expanding due to a preference for high-performance luxury vehicles and a growing fleet age averaging 7 years.

The Shift to Precious Metals

To meet tightening fuel economy standards—where modern combustion systems have achieved a 10% efficiency improvement—OEMs are aggressively shifting away from traditional nickel-copper plugs. Approximately 45% of new gasoline vehicles are now manufactured with iridium or platinum plugs. Iridium plugs are the fastest-growing segment because they offer the extreme hardness (six times harder than platinum) required to withstand the high pressures of turbocharged Direct Injection (GDI) engines while offering service intervals of 100,000 to 120,000 miles.

Global Spark Plug Market Summary (2025 Data)

| Category | Key Stat / Trend | Leading Region / Segment |

|---|---|---|

| Market Valuation | $4.7 Billion (2025) → $7.1 Billion (2035) | Asia Pacific (Fastest Growth) |

| Dominant Product | Hot Spark Plugs (68% Share) | Urban Commuter / Two-Wheeler |

| Fastest Material | Iridium / Precious Metal | High-Performance / Turbo GDI |

| Key Drivers | Aging Fleet (12+ Years), Hybrids, Urbanization | Aftermarket Replacement |

| Top Players | Niterra (NGK), Bosch, Denso, Tenneco | Niterra holds ~31.2% Share |

Q&A: Market Trends

Q: Will electric vehicles kill the spark plug market?

A: Not immediately. While EVs reduce long-term demand, the rising number of Hybrid vehicles (HEVs/PHEVs) and the massive existing fleet of 1.45 billion ICE vehicles ensure steady growth through at least 2035.

Q: Which region is the most profitable for spark plug manufacturers?

A: Asia Pacific offers volume profitability due to the massive scale of two-wheeler and passenger car production in China and India. However, North America and Europe offer higher margins per unit due to the preference for premium Iridium and Platinum products.

Would you like me to do the same for the other three articles? I can also create a Tailored Report document that compiles all four articles into a single, formatted PDF or text file if you prefer to upload them as a document resource on your site.